By Chris Sloan

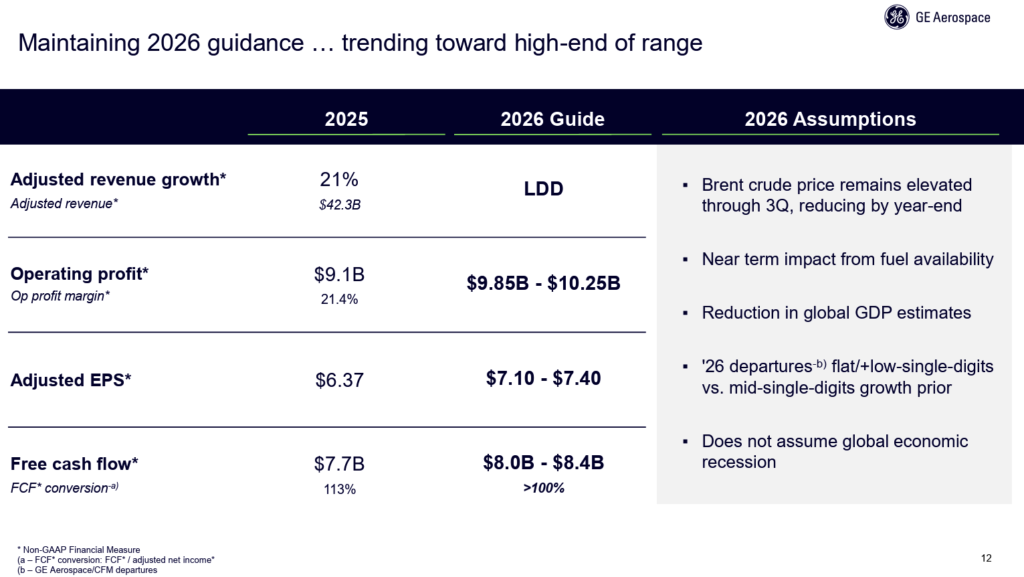

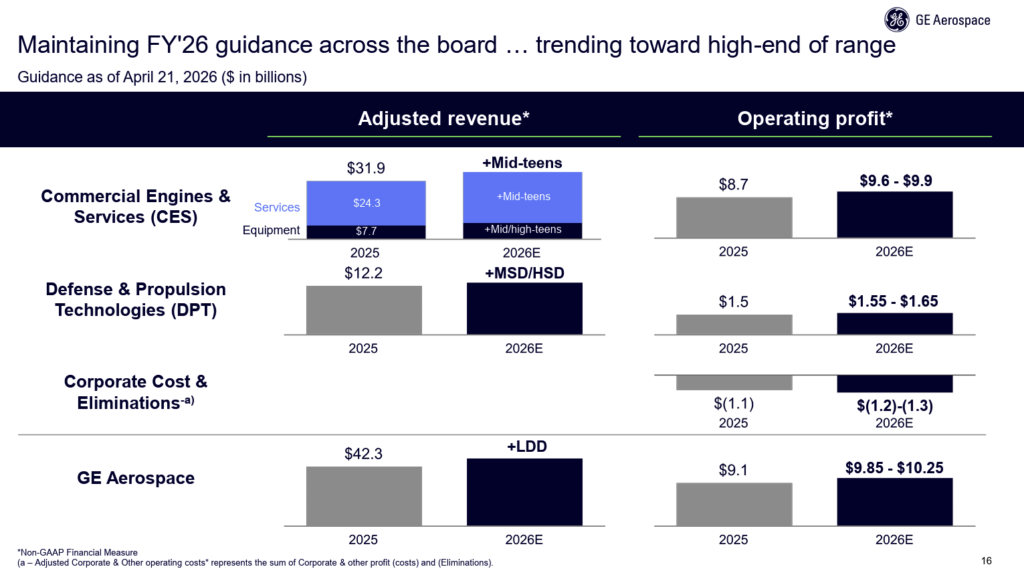

April 21, 2026, © Leeham News: GE Aerospace opened 2026 with a strong quarter, but the earnings call was dominated by the impact of the conflict in the Middle East following the launch of Operation Epic Fury on Feb. 28. Chief Executive Officer Larry Culp said the company was “embracing today’s reality,” even as performance remained solid. The late-quarter timing limited the impact on first-quarter results, but the disruption began to shape expectations for the balance of the year.

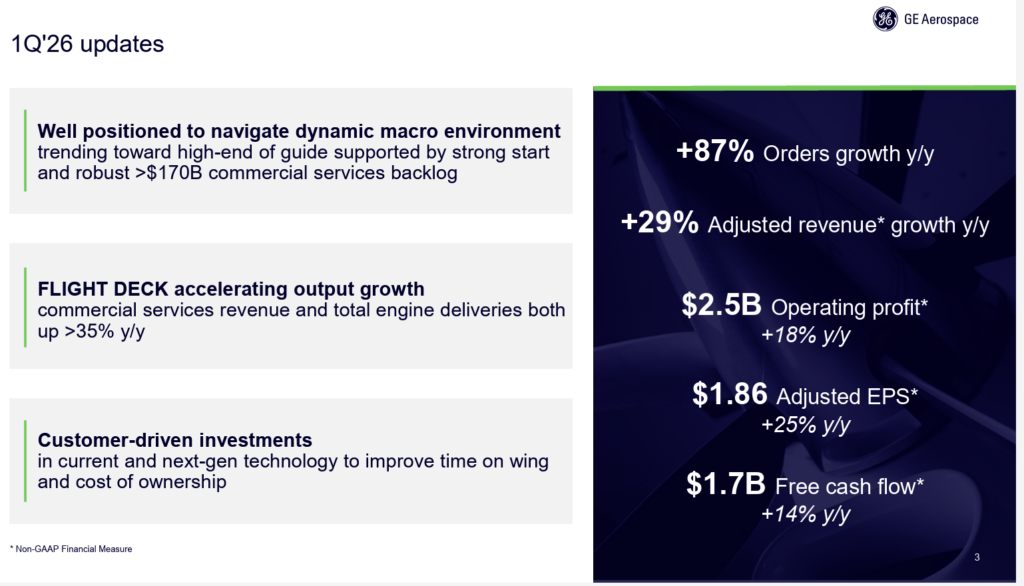

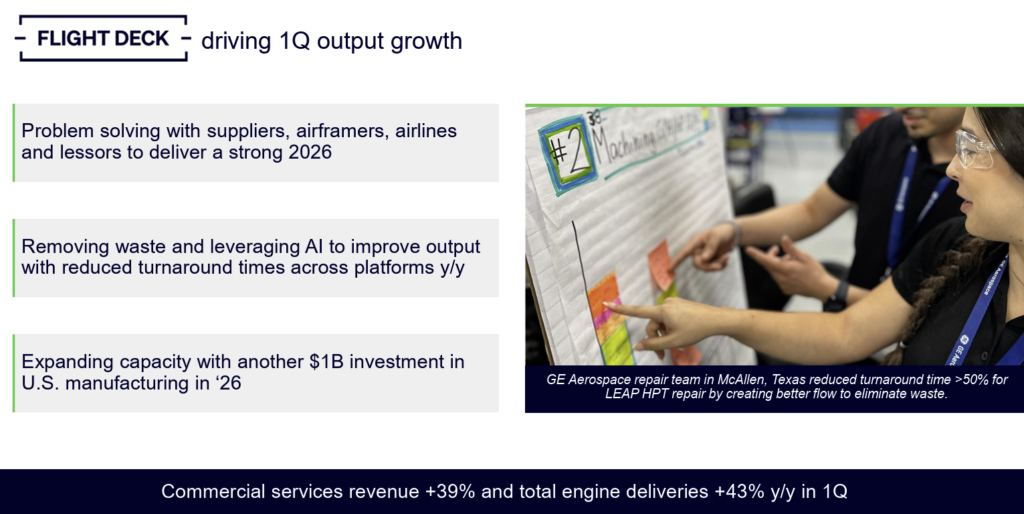

Culp pointed to a robust start, with orders up 87%, revenue rising 29%, and operating profit increasing 18%. Growth was led by Commercial Engines & Services (CES), with services revenue climbing 39% and total engine deliveries increasing 43%. The CEO credited FLIGHT DECK execution for improved output across programs including LEAP and GEnx.

Chief Financial Officer Rahul Ghai highlighted strength in equipment, with revenue up 20% and engine deliveries increasing 50%, including a 63% rise in LEAP units. Widebody deliveries also increased more than 25%, driven by GEnx, with additional contribution from GE9X ramp activity.

Iran War impacts air traffic

The conflict began to affect air traffic trends. Culp said global departures were up in the low single digits in the quarter, but down in the high single digits in the Middle East, which represented about 5% of total departures. For the full year, the company reduced its outlook to flat to low single-digit growth, down from prior mid-single-digit expectations, including a low double-digit decline in the Middle East.

GE Aerospace prepared for multiple scenarios as the situation evolved, with duration the key uncertainty. Culp said the company did not anchor to a single outlook and evaluated a range of potential outcomes depending on how long the disruption persisted. The CEO emphasized the backlog strength and a young, diverse fleet, including large installed bases of CFM56, LEAP, GE90, and GEnx, as important buffers against volatility.

The discussion turned to potential impacts on maintenance, repair, and overhaul (MRO), particularly if high fuel prices persisted. Bernstein Research flagged pressure on airlines—especially low-cost carriers—raising the risk of deferred shop visits or capacity reductions, particularly for older platforms such as the CFM56 and GE90. Newer, more fuel-efficient engines like LEAP were less affected.

Culp noted that services demand typically lagged changes in air traffic, suggesting any MRO impact would emerge over time rather than immediately. The CEO pointed to the company’s large shop-visit backlog as a source of resilience, even as airlines began adjusting near-term plans.

Ghai added that customers remained eager to return capacity despite near-term disruptions, describing the environment as fluid but not yet showing structural demand weakness.

Defense work offsets commercial

Defense provided a clear offset. Culp said military engine utilization has increased since March, supporting future aftermarket demand across platforms such as the T700, which powers Black Hawk and Apache helicopters, as well as engines supporting the F-15EX, F-16, B-1, and B-2 fleets. Defense & Systems deliveries rose 24% amid continued program activity.

GE Q1 2026 Earnings Slide

CES Services: Backlog Strength Anchors Aftermarket Resilience

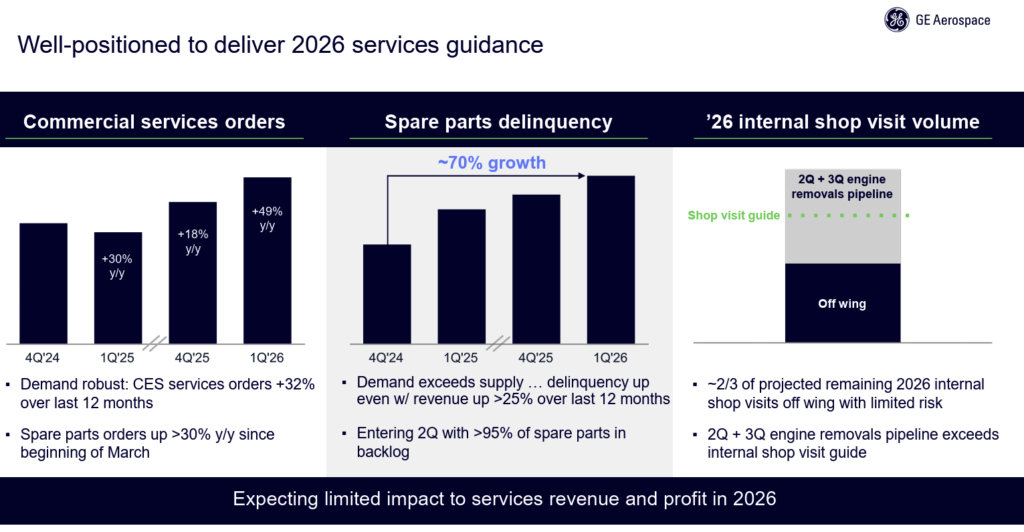

Commercial Engines & Services (CES) remained the core profit driver, supported by a rapidly expanding backlog and sustained demand. Culp said Commercial Services backlog increased by nearly $30bn since the end of 2024, “providing visibility into multi-year demand.” Orders grew more than 30% over the past 12 months, including 49% growth in the first quarter.

Demand for spare parts continued to exceed supply. Culp noted spare parts orders were up more than 30% year-over-year since March, even as revenue has grown more than 25% over the last five quarters, with “demand continues to exceed supply.” Delinquency increased roughly 70% since the end of 2024, leaving more than 95% of second-quarter spare parts revenue already in backlog.

Internal shop visits, which accounted for about 60% of Services revenue, provided additional visibility. Culp said roughly two-thirds of 2026 shop visits were already off wing or awaiting induction, with the pipeline of removals in the second and third quarters “exceeding our shop visit guide,” helping de-risk the outlook.

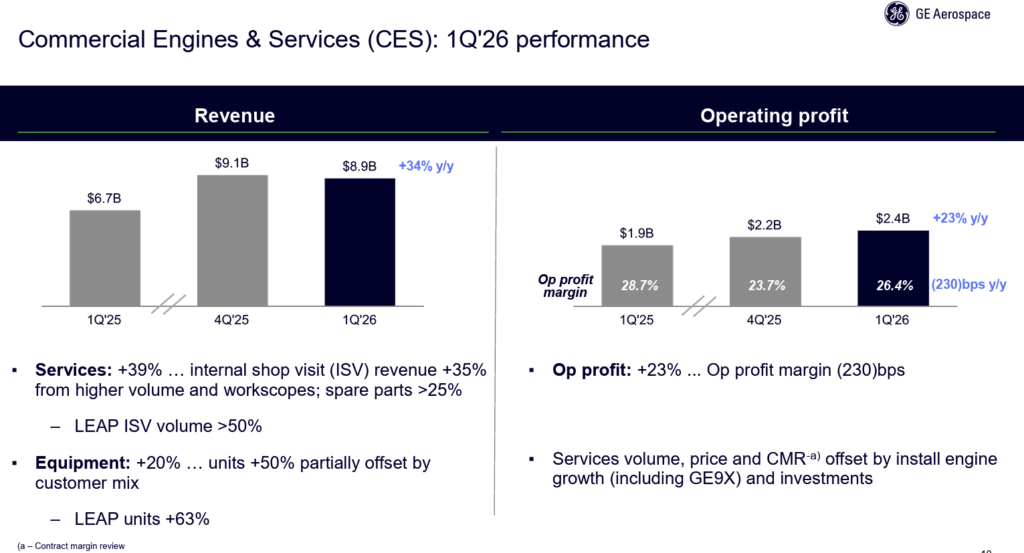

Ghai said CES revenue increased 34% in the quarter, with services up 39% and shop-visit revenue rising 35% due to higher volumes and a broader work scope. LEAP shop visits grew more than 50%, while spare parts sales increased more than 25%, supported by improved material availability and external demand.

Retirement rates below expectations

Analysts focused on whether the conflict could lead to reduced utilization or accelerated retirements of older engines such as the CFM56 and GE90. Ghai said retirement rates remained below expectations, with CFM56 retirements “sub-1%” in the first quarter versus a roughly 2% assumption for 2026. There was no meaningful increase in parked aircraft, and retirements were “lower than what we experienced in the fourth quarter.”

Ghai emphasized that GE’s scale helped “dampen the volatility,” with exposure to about 75% of narrowbody and 55% of widebody cycles. The fleet also remains relatively young, with a third of CFM56 engines yet to have a first shop visit and two-thirds not yet to have a second, while about 70% of GE90 engines have not reached a second shop visit.

Culp acknowledged that any sustained decline in departures would flow through to Services “with a lag.” Ghai added that any impact would likely be “a push out of demand versus a disruption,” as airlines defer maintenance activity rather than cancel it, depending on how the situation evolves.

Bernstein Research cautioned that prolonged high fuel prices could pressure midlife aircraft and aftermarket activity, particularly for less fuel-efficient engines. However, large industry backlogs for shop visits were expected to provide near-term insulation, even if airlines begin prioritizing newer platforms.

GE Q1 2026 Earnings Slide

CFM56: Legacy Fleet Provides Stability

The CFM56 remained a cornerstone of GE Aerospace’s Services outlook, providing durability even as market conditions shifted. Culp said “about two-thirds of the fleet is yet to undergo a second shop visit,” with utilization remaining stable. That dynamic continued to support steady aftermarket demand for the program.

The scale and maturity of the CFM56 installed base continued to underpin Services’ resilience. With a large portion of the fleet still in its maintenance cycle, the engine remained a consistent driver of shop-visit activity despite broader concerns about legacy platforms.

At the same time, emerging durability and supply constraints on next-generation narrowbody engines were becoming a growing industry issue. Southwest Airlines, among other customers, was facing a potential shortage tied to life limits on high-pressure turbine disks, capped at 10,000 cycles, with more than 40 aircraft approaching 8,000 cycles. Replacement hardware with higher durability was not expected to be available in meaningful volumes until the second half of 2026, creating a near-term supply gap.

The risk was operational. Without sufficient spare engines, airlines could be forced to ground aircraft or adjust schedules, particularly during peak periods. While not yet reflected in GE’s results, these constraints pointed to downstream effects that could influence utilization patterns and the timing of maintenance demand across the narrowbody fleet.

Supply Chain: Demand Outpaces Supply

Supply chain constraints remained a key operational challenge, with GE Aerospace openly acknowledging ongoing shortfalls. Culp said delinquency levels reflected “demand outstripping supply,” calling it a metric the company was “not proud of” as it continues to miss some customer delivery expectations. He added that eliminating delinquency remains a core operational goal, but “it’s going to take us a while yet” to reach that point.

The CEO emphasized that on-time delivery is a critical KPI (Key Performance Indicator) under FLIGHT DECK and cannot be ignored. Despite the gap, Culp pointed to continued improvement, with momentum building across both suppliers and internal operations. He said the company expects to reduce delinquency over time “regardless of the demand environment.”

From a supply standpoint, inputs are improving. Culp said key suppliers are delivering double-digit increases in output, both sequentially and year-over-year. He described GE’s approach as collaborative, noting that the company aims to be “problem solvers, not finger pointers,” with a focus on improving transparency and coordination across the supply base.

GE Q1 2026 Earnings Slide

Investments: Expanding Capacity to Support Growth

GE Aerospace is backing its growth plans with continued investment in manufacturing and the supply chain. Culp said the company plans to invest $1bn in U.S. manufacturing sites and its supplier base for the second consecutive year, aimed at accelerating engine deliveries and increasing production of parts that extend time-on-wing.

An additional $100mn is being directed toward external suppliers, funding equipment and tooling to expand capacity. Culp said these actions are already driving “meaningful progress” in improving both services and equipment output, supporting the company’s ability to meet sustained demand.

OE Growth: Deliveries Rising, Profit Inflection Ahead

Original equipment (OE) growth continued to build, supported by higher deliveries and improving services contribution. Ghai said the positive “drop through” from services was being offset by OE growth in the near term, with LEAP margins improving but broader headwinds expected to peak around 2028. Beyond that point, he said the business is positioned for “accelerated profit and margin expansion.”

GE Q1 2026 Earnings Slide

LEAP: Production Growth Drives Volume

LEAP remained the primary driver of OE growth, with production increases supporting both narrowbody programs. Culp highlighted continued commercial momentum, including American Airlines committing to more than 300 LEAP-1A engines, with options for 200 more, for A321neo and A321XLR aircraft. The CEO described it as an extension of a long-standing partnership as the airline expands its fleet.

Ghai said LEAP deliveries are expected to increase by about 15% for the year, with growth driven primarily by installed engines rather than spares. Both categories are increasing, but fleet expansion remains the dominant driver of volume.

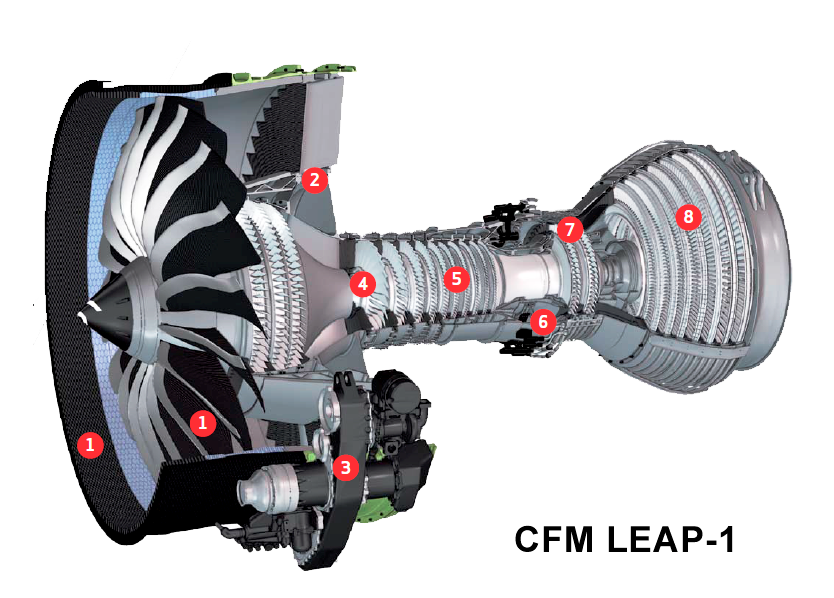

CFM LEAP-1 engine Image: Safran

GE9X: Certification Advances, Durability Issue Addressed

The GE9X program continued to progress through certification for the Boeing 777X, with entry into service still expected in early 2027 and a potential first delivery to Lufthansa by the end of 2026. The program has advanced to TIA Phase 4 of 5, with flight testing ongoing and production continuing as engines accumulate.

Culp said there was “no change on schedule” or expected losses while addressing a durability issue involving a mid-seal discovered during a shop visit on a flight test engine. The crack, identified in a component originally certified in 2020, had been seen before, with root cause understood and a modification being finalized. GE is updating tooling and working with suppliers to incorporate the fix into the production system.

The company has built a substantial inventory of GE9X engines, with more than 1,000 units on order, and is continuing assembly through the modification stage. Deliveries are expected to be weighted toward the second half of the year as the updated configuration is introduced. Ghai added that GE9X losses are expected to peak around 2028, alongside a targeted 50% reduction in program costs.

Cutaway view of the GE9X – The world’s largest and most powerful commercial turbofan, capable of delivering over 134,000 lbs of thrust. Designed for the Boeing 777X—the world’s largest twin-engine jet. Courtesy: GE Aerospace

GEnx: Widebody Franchise Strengthens

The GEnx program continued to benefit from renewed widebody demand and strong competitive positioning. GE Aerospace dominates the Boeing 787 engine market, with roughly 78% overall share and a 99% win rate on new orders since 2023, driven largely by the engine’s reliability.

The GEnx-1B powers about two-thirds of the active 787 fleet, with more than 70% of recent orders selecting GE. Culp highlighted major commitments from United Airlines for 300 engines and Delta Air Lines for 60 engines with options for 60 more, marking Delta’s first selection of the platform.

Related

source