By Chris Sloan

![]()

Analysts pointed to RTX’s diversified structure as a key advantage in this environment. Vertical Research Partners said, “while investors may not be huge fans of diversification, RTX’s 1Q results have shown that sometimes it can work out,” citing “aftermarket growth at Pratt, OEM growth at Collins, and munitions growth at Raytheon” as drivers of strong performance, with the latter “driving the upside to the 2026 guidance.”

As a prime contractor across propulsion, avionics and defense systems, RTX sits at the center of the defense response. Demand for defense products and services remained robust, with increased focus on munitions production, replenishment cycles and sustained operational tempo across U.S. and allied forces.

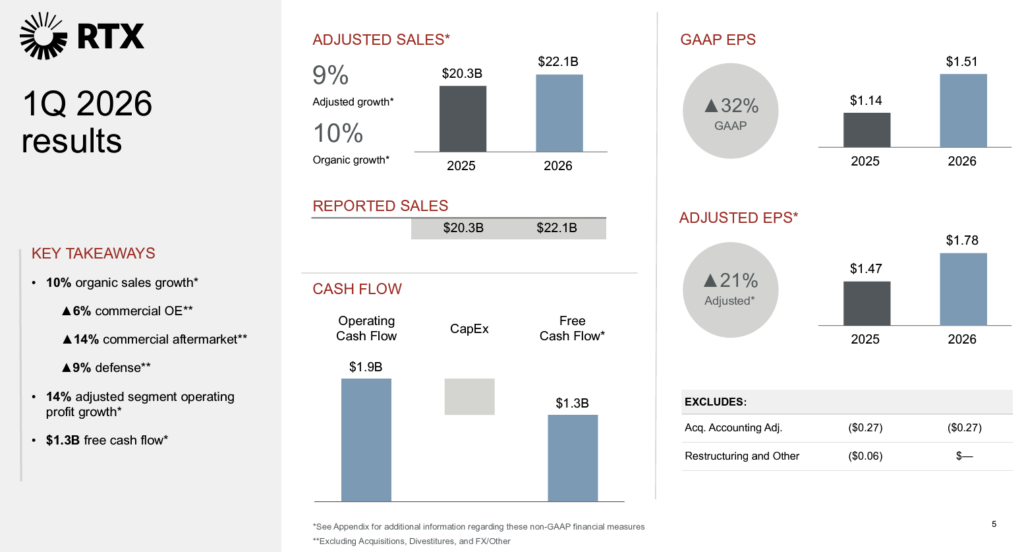

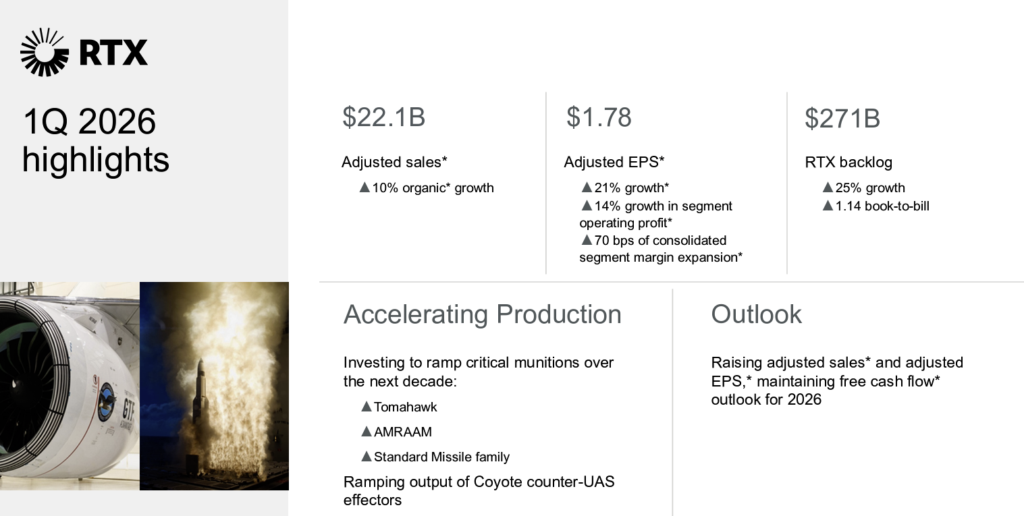

President and Chief Executive Officer Christopher Calio said adjusted sales were $22.1bn, up 10% organically, with growth across all three segments. Adjusted EPS of $1.78 increased 21% year-over-year, driven by 14% growth in segment operating profit, while free cash flow reached $1.3bn, up $500mn from a year ago.

Orders reflected this strength. Calio shared the book-to-bill was 1.14, with backlog reaching a record $271bn, up 25% year-over-year, supported by both commercial and defense awards. The defense side, particularly munitions and systems, was a key contributor to growth and visibility.

RTX Q1 2026 Earnings Slide

Commercial Aftermarket: Limited Near-Term Impact from Traffic Shifts

RTX continues to see resilience in its commercial aftermarket despite early signs of airline capacity adjustments. Calio said commercial backlog increased 30% year-over-year, with strength across both OE and aftermarket, including GTF wins such as VietJet selecting engines for 44 additional aircraft.

The CEO said that while “the environment is dynamic,” underlying demand for OE and aftermarket services remains durable. Commercial OE was in line with expectations in the first quarter, with continued production ramps expected across multiple platforms through the remainder of the year.

Traffic trends remained stable through the quarter. Calio said RPK growth was “solid” despite disruption in the Middle East, while aircraft retirement rates stayed below historical levels, with V2500 retirements in line with expectations. He emphasized the long-cycle nature of the business, noting demand for new aircraft and services remains intact despite near-term volatility.

The discussion focused on how changes in air travel could affect Collins and Pratt aftermarket demand. Calio said airlines are adjusting capacity, including retiring older aircraft, but noted that much of RTX’s aftermarket exposure is not tied to those platforms. As a result, near-term retirements are not expected to materially impact maintenance demand.

At Pratt & Whitney, the aftermarket is anchored by the V2500 and GTF. Calio said the V2500 remains a “very, very young fleet,” with about 50% of engines yet to undergo a first or second shop visit, supporting continued shop visit demand. First-quarter shop visits were strong and expected to remain so through the year.

The GTF adds another layer. While it is “the most fuel efficient,” Calio said the company is still working through fleet management and durability-related issues, with engines continuing to cycle from parked status into MRO shops. This dynamic is supporting aftermarket activity even as airlines adjust operations.

Chief Financial Officer Neil Mitchill said increasing numbers of engines coming out of warranty are also supporting demand. He noted these aircraft “will continue to fly even in a slightly depressed environment,” providing stability to aftermarket revenue streams.

Mitchill added that RTX is not changing its 2026 outlook for commercial OE or aftermarket. While the company is closely monitoring fuel prices, availability constraints and airline behavior, he said RTX has “pretty good line of sight to the demand” across its portfolio.

Defense: Conflict Touted as Major Driver of Demand

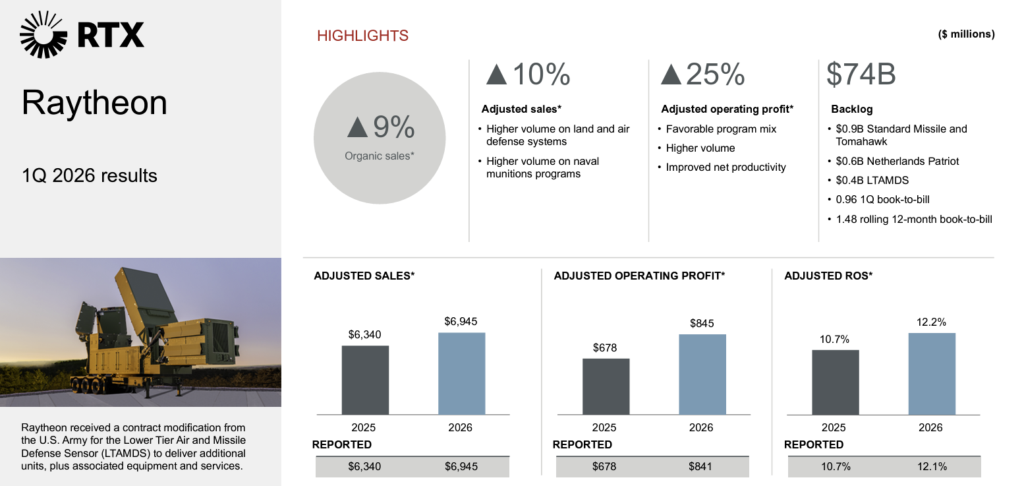

Defense is not typically a focus of LNA or even RTX earnings calls, but it was an outsized focus this quarter given the conflict in the Middle East following Operation Epic Fury. Management repeatedly touted defense demand as a key driver, particularly across Raytheon, with additional strength in Pratt & Whitney’s military portfolio.

Calio said the Department of Defense is prioritizing “munitions depth,” integrated air and missile defense, and advanced counter-threat capabilities—areas where RTX is heavily positioned. He pointed to franchise systems such as Patriot, NASAMS, AMRAAM, Tomahawk, and the F135 engine as core to U.S. and allied defense architectures, with demand accelerating.

Counter-UAS capabilities were highlighted as a growing priority. Calio said the Coyote system is seeing “really, really strong demand” following strong field performance, with a new non-kinetic, reusable version capable of countering drone swarms and returning for redeployment. International demand is also increasing, as evidenced by recent approvals for foreign military sales.

Orders reflected the strength across the portfolio. Raytheon booked $6.6bn in the quarter, including Patriot and air and missile defense systems, while Pratt secured more than $3bn for F135 Lot 19 production. Collins added nearly $3bn in awards, including $1.7bn in mission systems and $400mn in avionics.

RTX is also accelerating production to meet demand. Calio pointed to five framework agreements with the Department of Defense covering key munitions programs, reinforcing long-term visibility as replenishment cycles build.

The company expects sustained growth. The CEO said these priority areas are likely to see “significant funding increases” in the 2027 U.S. defense budget and supplemental packages. Reflecting this momentum, RTX raised its full-year outlook for adjusted sales and EPS while maintaining free cash flow guidance.

RTX Q1 2026 Earnings Slide

Pratt & Airbus: Balancing OE Deliveries and Fleet Support

Tensions with Airbus over GTF engine availability remained a central issue, as Pratt & Whitney continued to balance production ramp-ups with supporting its in-service fleet. The challenge stems from allocating constrained materials between OE deliveries and aftermarket requirements tied to grounded aircraft from powder metal-related inspections.

Airbus continues to feel the strain. The OEM delivered just 114 aircraft in the quarter, including 81 A320neos, far below earlier ambitions, with its 75-per-month target now pushed to late 2027. Airbus CEO Guillaume Faury has been outspoken, saying the company is “very dissatisfied” and prepared to “enforce our contractual rights” if engine supply does not improve.

Calio said the first quarter reflected deliberate trade-offs. He noted the company was “allocating materials between MRO and original equipment,” which showed up in both sales and delivery performance. Despite this, RTX still expects OE sales to grow in the low single digits, with unit deliveries increasing mid- to high-single digits for the full year.

Shifting balance

The balance is expected to shift as the year progresses. Calio said RTX will “continue to see OE delivery step up throughout the year,” adding that by year-end the company expects to deliver a record number of GTF engines. He said delivery share will remain above program share, even as Pratt works to reduce AOG levels and support its installed base.

That shift comes with near-term margin pressure. The Chief Executive said “negative engine margin will ramp up over the next several quarters” as the company increases OE output while continuing to support fleet health. The priority remains reducing AOGs and “delivering to our end customer, Airbus,” while managing the mix between OE and MRO.

RTX is investing to relieve the bottlenecks. Calio pointed to capacity additions, including a new forging press in Columbus (GA), a new powder production tower in New York, and turbine airfoil ramp-ups in Asheville. He also highlighted MRO investments in Singapore, which are being replicated across the network to support both OE and aftermarket demand.

Despite the tension, Calio emphasized the long-term partnership. He said discussions with Airbus are “always ongoing,” focused on “what’s going on industrially” and balancing the needs of fleet health and production. He added that the relationship spans decades and will continue to do so, with both sides working “in a constructive and transparent manner” to resolve current constraints.

RTX Q1 2026 Earnings Slide

Supply Chain: Progress Continues, No New Disruptions

Supply chain execution remains a critical focus as Pratt & Whitney supports both OE ramp-ups and aftermarket demand. Calio said the company has been “laser focused” on scaling key inputs, including structural castings, turbine airfoils, and other critical engine components.

He said progress is being made, with continued growth in the availability of these materials supporting production needs. Despite the scale of the ramp—feeding both OEM and aftermarket channels—Calio said the company is “not seeing anything new crop up,” signaling relative stability in the supply base.

The challenge remains one of volume. RTX is managing “pretty substantial” demand across both channels, but the absence of new disruptions suggests prior bottlenecks are gradually easing.

GTF: AOG Recovery Shows Progress, Time-on-Wing Remains a Gap

The GTF AOG (aircraft on ground) situation, now in its third year, remains a central issue for RTX, though there are signs of improvement. Calio said the fleet management plan remains “on track,” with PW1100 aircraft-on-ground levels down about 15% from the end of last year. The program also marked a milestone, reaching 10 years in service with more than 50 million flight hours and a backlog of about 8,000 engines.

Shop performance is improving and is the primary driver of recovery. Mitchill said PW1100 MRO output increased 23% year-over-year, following 35% growth in the prior year, with heavy shop visits up nine points and turnaround times improving about 20%. He said this “very, very good performance in the shop” is enabling the reduction in AOGs and supporting a continued downward trajectory.

Throughput across the system is building. The CFO noted inductions were up 7% sequentially from the fourth quarter, improving work-in-progress levels in the shops, while key inputs such as structural castings increased 10% year-over-year, and isothermal forging rose 18%. These gains are critical to sustaining higher MRO output and supporting fleet recovery.

Despite this progress, time on wing remains a key differentiator. Bernstein Research noted that current GTF engines are achieving roughly 10,000–12,000 cycles in benign environments and closer to 4,000 cycles in harsher conditions before shop visits. By comparison, LEAP engines are approaching 17,000 cycles in neutral environments and about 8,000 cycles in harsher regions, highlighting a meaningful durability gap.

Trade-off

The trade-off is efficiency. The GTF offers a 3%–4% fuel-burn advantage over LEAP, but it comes with more frequent maintenance and earlier shop visits. This tension between fuel efficiency and durability continues to shape airline operating strategies, particularly in an environment of elevated fuel prices.

The scale of the disruption remains significant. Bernstein estimates that grounded GTF-powered aircraft remain above 600, or roughly 30% of the fleet, with about two-thirds tied to powder metal-related inspections. Mitchill added that not all AOGs are engine-related, but acknowledged ongoing removals tied to durability issues beyond those related to powder metal.

RTX continues to manage the recovery through MRO throughput, material allocation, and fleet upgrades. Calio said balancing OE and aftermarket support is critical to “ensure the health of the overall fleet,” while the company recorded approximately $170mn of powder metal-related compensation in the quarter.

Pratt & Whitney GTF Engine Cutaway

GTF Advantage: Next-Generation Fix Targets Durability Gap

RTX is positioning the GTF Advantage as the long-term solution to the durability challenges that have defined the current GTF fleet. Calio said the engine achieved aircraft-level certification during the quarter, keeping the program “on track for entry into service later this year,” a key milestone as Pratt moves toward a transition from the current PW1100G.

The certification pathway has progressed steadily. The engine received FAA type certification in early 2025, followed by EASA validation later that year, and most recently EASA aircraft-level certification for the A320neo family in April 2026—clearing the way for initial deliveries.

The GTF Advantage represents a significant redesign, particularly in the hot section, aimed at addressing known durability issues. The upgraded engine delivers 4%–8% more take-off thrust, improves fuel burn by about 1%, and is designed to potentially double time-on-wing compared to earlier GTF variants. It is also fully interchangeable with existing engines, allowing operators to integrate it into current fleets without operational disruption.

The CFO admitted the improved capability comes with “a little bit more cost,” but added that pricing adjustments are expected to offset much of that impact. As a result, he does not expect “a lot of headwind on a per-engine basis” as the Advantage ramps over the next several years, even as Pratt continues to see negative margins on OE deliveries.

The near-term financial profile remains mixed. Mitchill said OE margins will face a couple of hundred million dollars of headwind this year, though the first-quarter impact was minimal. At the same time, the aftermarket continues to strengthen, with GTF MRO output up more than 20% and margins in the low double digits, driving improved profitability as shop visit intensity increases.

Execution risk remains. Bernstein Research said the key question is how effectively the GTF Advantage will resolve legacy durability issues beyond powder metal, including hot section wear and other operational challenges. While the redesign is extensive and based on testing, the firm noted that Airbus has been cautious about the rollout, with certification for certain variants still pending and the production ramp expected to be gradual.

The transition will take time. Bernstein expects a full cutover from the current GTF to the Advantage by the end of 2027, though early production rates appear slow. That suggests the benefits—particularly improved time on wing—will phase in gradually rather than provide an immediate step change in fleet performance.

Hot Section Plus: Retrofit Path to Faster Durability Gains

RTX is also introducing a retrofit solution for the existing GTF fleet to accelerate durability improvements ahead of the full GTF Advantage rollout. Calio said the newly certified GTF Advantage “paves the way” not only for new engine deliveries, but also for the introduction of the Hot Section Plus upgrade into the installed base.

The Hot Section Plus package is effectively the retrofit version of the Advantage. Calio said the upgrade includes roughly 30 to 35 parts and is expected to deliver “almost 95% of the durability benefits” of the new engine. The package is scheduled to be introduced into MRO later this year, ahead of broader entry into service of the GTF Advantage itself.

This creates a near-term pathway to improve time-on-wing across the fleet without waiting for a full engine replacement. By pushing these upgrades through shop visits, RTX can begin addressing durability gaps and reducing maintenance intensity more quickly across the installed base.

Pricing will reflect the value of the upgrade. Calio said the company has “invested significantly” in the design and testing of the Advantage and intends to capture value from that investment while tailoring its implementation to customer needs and operating environments.

The strategy reinforces the broader recovery plan. By combining retrofit upgrades with new engine deliveries, RTX aims to close the durability gap and improve fleet performance more quickly, while supporting both aftermarket growth and long-term customer economics.

Legacy Engines: Aftermarket Strength Faces Fuel Pressure Risk

RTX’s legacy engine portfolio continues to provide meaningful aftermarket revenue, though long-term trends remain mixed. The V2500 remains the key contributor, underpinning much of Pratt & Whitney’s legacy commercial engine profitability.

Mitchill said the V2500 fleet is still relatively young, with about 50% yet to see a second shop visit and 15% not having has a first, supporting continued demand. Shop visits were running at about 800 for the year, in line with expectations, with strong visibility into the pipeline despite a material-constrained environment.

Durability continues to support utilization. Mitchill said the V2500 “performs well,” with low expected retirement rates of around 1%–2%, suggesting airlines will continue operating these aircraft even amid higher fuel prices. This underpins steady aftermarket demand in the near term.

However, analysts flagged a growing risk if fuel prices remain elevated. Bernstein Research said nearly 50% of Pratt’s legacy commercial engine aftermarket revenue is tied to platforms such as the V2500, PW2000, and PW4000, with the V2500 representing the largest source of profit. Sustained high fuel prices—now more than double 2025 levels in some regions—could pressure airline profitability and lead to reduced flying or earlier retirements of less fuel-efficient aircraft.

The concern is tied to fleet behavior. Bernstein Research noted that in periods of excess capacity, airlines tend to prioritize newer, more fuel-efficient aircraft while parking older platforms, which could impact aftermarket demand for engines such as the V2500, CFM56, Trent 700, and GE90.

Other legacy platforms play a smaller or declining role. Mitchill said the PW2000—powering the Boeing 757—is “not a major driver,” while the PW4000, which powers aircraft including the Boeing 747-400, 767, 777, McDonnell Douglas MD-11 and Airbus A300-600, is in a “structured decline” that has been planned for several years.

In the near term, strong MRO backlogs provide insulation. Bernstein Research said demand for shop visits remains well above supply, with constrained capacity supporting pricing and utilization across the aftermarket. But if elevated fuel prices persist for an extended period, the impact on midlife aircraft and maintenance activity could become more pronounced.

A Pratt & Whitney MRO Facility Image: RTX

Pratt & Whitney: Aftermarket and Military Drive Profit Growth

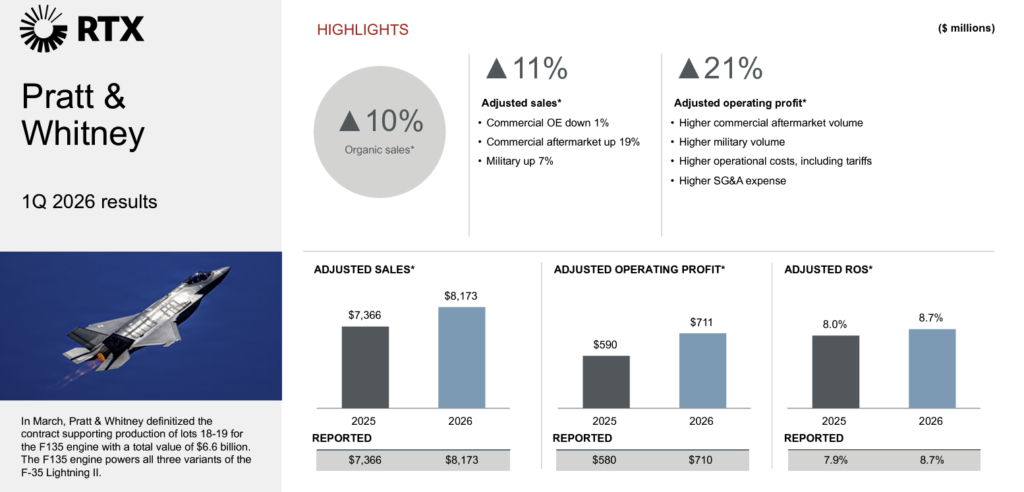

Pratt & Whitney delivered solid growth in the quarter, supported by strength in commercial aftermarket and military programs. Vice President of Investor Relations Nathan Ware said adjusted sales were $8.2bn, up 11% on an adjusted basis, or 10% organically.

Commercial OE sales were down 1% and in line with expectations, reflecting lower engine deliveries in the quarter. However, RTX continues to expect mid- to high-single digit growth in large commercial engine deliveries for the full year.

Profitability improved meaningfully. Adjusted operating profit reached $711mn, up $121mn year-over-year, driven by higher commercial aftermarket and military volumes. Margins expanded by 70 basis points despite a 50-basis-point headwind from tariffs, with higher SG&A and operational costs partially offsetting the gains.

Looking ahead, Pratt & Whitney expects continued growth. Ware said full-year sales are projected to increase at a mid-single digit rate, with operating profit expected to rise by $225mn to $325mn versus 2025, supported by ongoing aftermarket recovery and defense demand.

Collins Aerospace: OE Growth Offsets Mix and Tariff Pressures

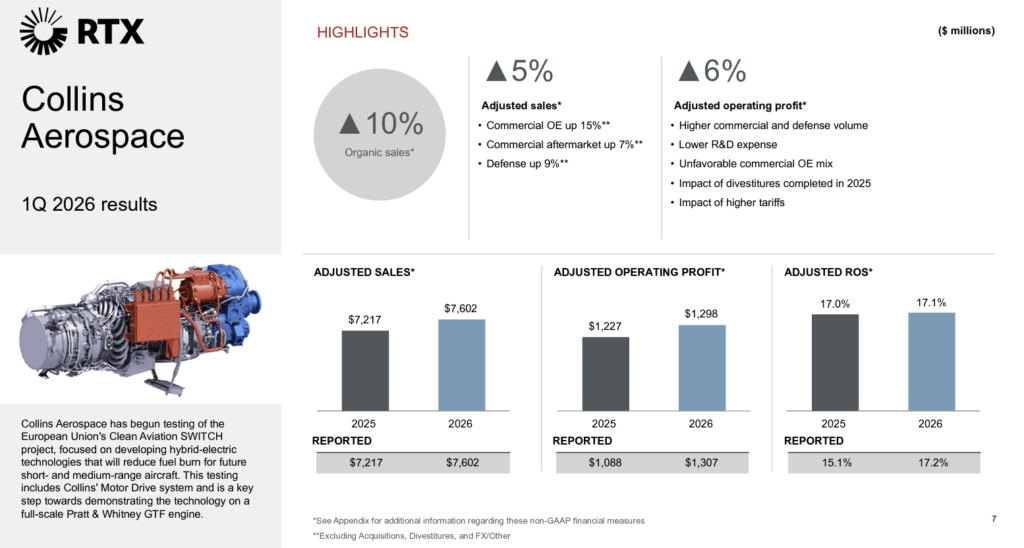

Collins Aerospace delivered a strong start to the year, with growth across both commercial and defense channels. Ware said sales were $7.6bn, up 5% on an adjusted basis and 10% organically, driven by higher volumes across the portfolio. Commercial OE sales increased 15%, supported by both narrowbody and widebody production, while commercial aftermarket rose 7%, led by provisioning, parts, and repair.

Profit growth continued despite headwinds. Adjusted operating profit reached $1.3bn, up $71mn year-over-year, with margin expansion of 10 basis points despite a 130 basis point impact from tariffs. Gains from higher volume and lower R&D were partially offset by unfavorable OE mix and the impact of prior divestitures.

Mitchill said Collins is managing through a shifting mix as OE volumes increase. He noted the business is “taking on more and more OE,” which creates a margin headwind, particularly as widebody production ramps, but said Collins continues to deliver margin expansion through cost control and operational discipline.

Widebody production remains a key driver. Bernstein Research highlighted planned increases in Boeing 787 and Airbus A350 output, two high-value platforms for Collins, which are expected to support top-line growth and operating leverage over time.

Aftermarket remains a watch point. Bernstein Research said interiors and avionics upgrades are more discretionary and could soften in a downturn, while wheels and brakes are tied more directly to flight hours and utilization. A reduction in flying, particularly for older aircraft, could put downward pressure on demand in these segments.

Near-term performance

Near-term performance remains solid. The CFO disclosed interiors posted low-teens growth in the quarter, with “good trajectory” and visibility into mods and upgrades for the remainder of the year, despite some certification timing on bespoke programs.

Collins is also investing in future growth. Calio said the business launched a capacity expansion effort tied to a recently awarded FAA radar contract and broader air traffic modernization opportunities.

Looking ahead, RTX expects continued steady growth. RTX’s VP of Investor Relations said Collins is projected to deliver mid-single-digit sales growth on an adjusted basis and high-single-digit organic growth, with operating profit expected to increase by $425mn to $525mn in 2026.

RTX Q1 2026 Slide

Innovation and Investment: Automation and Data Drive Throughput

RTX continues to invest in automation and digital capabilities to improve throughput and reduce costs across its operations. At Pratt & Whitney’s MRO facility in Singapore, advanced robotics is now assembling high-pressure compressor rotors, delivering 100% first-pass yield and cutting assembly time by 50%.

Calio said the company is expanding these efforts, including further automation of engine assembly and core stacking for the low-pressure compressor. These initiatives have already driven an 80% increase in output at the Singapore facility over the past two years, with similar capabilities now being deployed across the broader MRO network.

Digital tools are also playing a larger role. Calio said RTX expects to connect 60% of its annual manufacturing hours to its proprietary data and analytics platform by year-end, enabling faster decision-making and more efficient operations. The platform is also being integrated with the commercial installed base to enhance predictive maintenance.

Collins is already applying these capabilities. The CEO noted that the wheels-and-brakes business is using real-time data to better manage service life and inventory, reducing costs under its long-term service agreements.

RTX is also investing in physical capacity. He highlighted a $200mn investment in Pratt’s Columbus (GA), which supports both GTF and F135 programs. The expansion will increase output of critical components such as rotating compressor and turbine discs, supporting both OE production and aftermarket demand.

Next-Generation Propulsion: Hybrid Electric Advances

RTX continues to advance next-generation propulsion, focusing on hybrid-electric systems for regional aircraft. Calio said a cross-company team spanning Pratt & Whitney, Collins Aerospace, the RTX Research Center, and RTX Ventures is making “significant progress” on these technologies.

During the quarter, the company successfully operated a turboprop demonstrator propulsion system and battery pack at full power. The system combines a thermal engine from Pratt, a 1-megawatt electric motor from Collins, and a 200-kilowatt battery supported by RTX Ventures.

Calio said the architecture is expected to deliver about a 30% improvement in fuel efficiency for regional aircraft. The effort reflects RTX’s broader strategy of leveraging capabilities across its businesses to develop next-generation propulsion solutions.

Tariffs: Clawbacks Pending, Outlook Unchanged

Tariffs remain a moving piece of the financial outlook, but RTX is not changing its expectations for the year. Mitchill said there is “really no change” to the full-year tariff impact, with the company still expecting about a $75mn year-over-year tailwind as mitigation efforts take hold.

The policy landscape has shifted. Prior AIPA tariffs have been overturned and replaced with Section 122 and Section 232 measures, but Mitchill said that “on balance, the tariff impact is about the same” for RTX.

The bigger opportunity lies in potential refunds. Mitchill said the company has paid about $500mn in tariffs under the previous regime and expects to pursue clawbacks as the government begins the refund process.

For now, RTX is taking a conservative stance. He declared that no income from potential refunds has been recorded or included in guidance, adding that “if it improves, you’ll see it in the bottom line.”

Financials: Defense Strength Lifts Outlook, Commercial Mixed

RTX delivered a strong overall financial performance in the quarter. Adjusted segment operating profit increased 14% to $2.9bn, reflecting broad-based growth across the portfolio.

Growth was driven across all channels. Mitchill said commercial OE rose 6%, commercial aftermarket increased 14%, and defense grew 9%, with a favorable mix and higher volumes supporting profit expansion.

Productivity was a key contributor. Mitchill boasted the company achieved double-digit growth in both organic sales and segment profit with only a 1% increase in headcount, while consolidated segment margins expanded by 70 basis points, more than offsetting tariff headwinds.

RTX raised its full-year outlook, led by strength at Raytheon. Mitchill remarked the company increased its sales range by $500mn, now expecting $92.5bn–$93.5bn, with organic growth of 5%–6%. Defense is now expected to grow mid- to high-single digits, an increase from prior expectations, while commercial OE and aftermarket outlooks remain intact.

RTX Q1 2026 Slide

Earnings guidance also moved higher. Mitchill said adjusted EPS increased by $0.10 at both ends of the range, driven by stronger defense performance and favorable below-the-line items such as lower interest expense.

Analysts pointed to broad-based strength. Vertical Research Partners said results came in “ahead of the consensus,” with particularly strong free cash flow performance, while highlighting complementary trends across the portfolio with Collins OE strength and Pratt aftermarket growth.

J.P. Morgan said results were “strong across the board,” noting that Pratt drove the most upside in the quarter, while Raytheon and Collins also performed ahead of expectations. BNP Paribas’ Matthew Akers echoed that view, pointing to Pratt as the primary driver of upside and noting that overall results exceeded forecasts.

Melius Research upgraded RTX, citing its balanced exposure to both defense and commercial aerospace. The firm said demand for Raytheon’s missile and air defense systems is “arguably insatiable,” while defense growth at Pratt and Collins should help offset potential pressure in commercial aftermarket tied to higher fuel prices.

RTX Q1 2026 Earnings Slide

Related

source