By Karl Sinclair

![]()

He elaborated further on what the war means financially for the corporation.

“Let me give you a couple of examples of areas where I think this new defense budget is going to benefit us as well. We see $5bn in the budget for F-47. Increasing KC-46 production, $4bn. F-15EX, $3bn. The enhanced strategic SATCOM of $2bn. Massive increases in weapon systems as well. If you look at the backdrop of this, while it is funding new capability, it is really funding additional production of existing systems, which should be low risk for us,” he said.

While the defense sector appears to be the financial beneficiary of the conflict, Boeing sees little downside to commercial orders in the Middle East region.

“Fourteen percent of our unit backlog is in the Middle East for customers, but two-thirds of that backlog delivers out in 2030 and beyond. We have pretty good ability to re-sequence airplanes in the 12 to 18-month timeframe, so I think we will be okay,” he explained.

Boeing Commercial still in the red

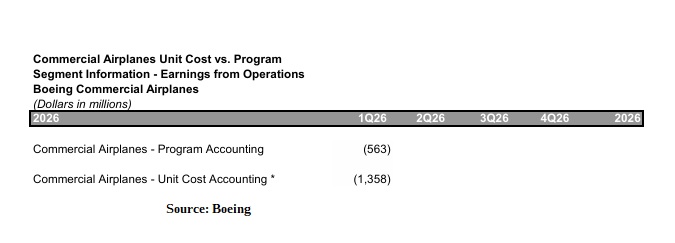

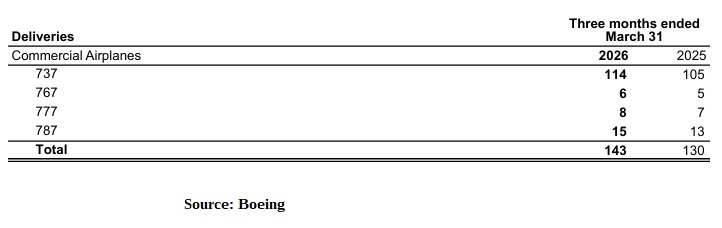

Despite increasing deliveries and revenues at the commercial division, Boeing experienced an uptick in losses at Boeing Commercial Aircraft (BCA) in 1Q2026. BCA handed over 143 aircraft to customers during the quarter (130 in 2025), and revenues grew to $9.203bn ($8.147bn in 2025). This resulted in a loss from operations of $563m for the period ($537m in 2025).

The reported figures were generated using program accounting. When the numbers are tallied on a unit-cost basis, the losses deepen even further.

Boeing reports that the 737 MAX program has now stabilized production at 42/mo, with the MAX 7 and MAX 10 variants certified sometime in 2026 and deliveries beginning in 2027.

The 787 program has also stabilized at a rate of 8/mo, with Boeing reporting that $1.275bn has been spent on property, plant, and equipment (PP&E) in St. Louis (MO) and Charleston (SC), home of the Dreamliner final assembly line.

Supply chain, certification impacts BCA

The program is facing difficulties with cabin interiors, according to Ortberg. “We’ve been struggling with getting the seat certifications completed for the new cabin configuration. So, if it’s a new seating configuration, typically with doors, this has been an area where we’ve struggled. We’ve got a fair number of 787s that are held up, that are actually built, that are held up now to get seat certifications.”

Boeing is also struggling with supply chain snarls with powerplants.

“In terms of the supply chain, other supply chain performance, it’s been a tough quarter in terms of engine deliveries for us. They’ve fallen behind a little bit. We do have a recovery plan on engines. So, we’ve got to stay on that recovery plan to allow us to get to the next increase of 10 later on in the year,” he elaborated.

The investments in the Charleston FAL will enable BCA to increase 787 production to 14/mo, while the new North Line in Everett (WA) will bump 737 MAX production to 47/mo this summer.

The 777X program has received FAA approval to begin the TIA 4A Phase of flight testing, with first delivery expected in 2027.

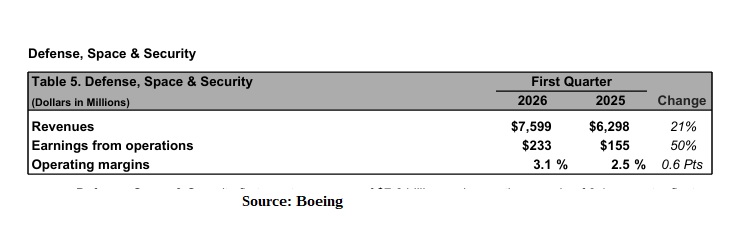

BDS in the black again

Long heralded as a money-pit, Boeing Defense Space and Security (BDS) posted another profitable quarter, earning $233m on revenues of $7.599bn.

This was an increase over the same period last year, when it earned $155m on $6.298bn in sales.

While a 3.1% profit margin may not seem like an extraordinary financial result, it is undoubtedly welcome news at a division that has consistently posted losses over the past five years.

In the fourth quarter of 2025, BDS posted a loss of $507m for the period ($128m loss for FY2025), driven by a $600m write-off on the KC-46 tanker program, which has been beset with problems from the get-go. Losses on the program have now surpassed $8bn.

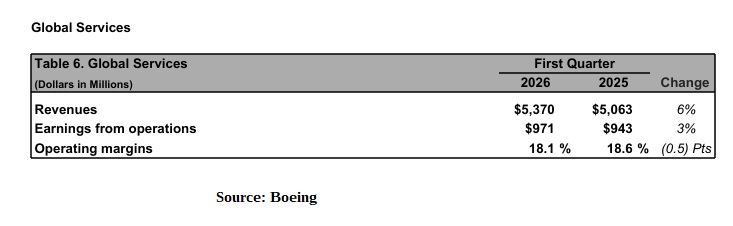

Boeing Global Services (BGS) performed well during the quarter, posting revenues of $5.37bn and earnings of $971m, for a margin of 18.1%.

Boeing declared that revenues increased due to “higher government volume,” which would explain the jump from $5.209bn in 4Q2025 revenues.

This is despite the revenue loss from the 2025 sale of Jeppesen (Digital Aviation Solutions), which led to a $9.6bn cash injection in the last quarter.

Fiscal Responsibility

During the quarter, Boeing repaid $6.95bn to lenders, using proceeds from the spin-off of Jeppesen. The result is that the combined short and long-term debt load dropped to $47.209bn, from $54.098bn, at the end of 4Q2025. This resulted in interest expense decreasing to $616m from $708m a year ago–almost $100m savings.

Cash and equivalents (along with short term investments) fell from $29.4bn to $20.905bn, during the quarter.

Boeing still has a short-term debt and current portion of long-term debt obligation of $2.855bn to repay within the 12 months.

Deferred Production Costs

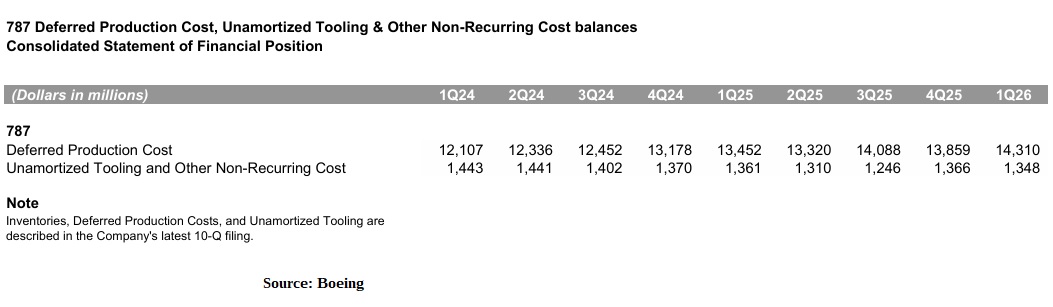

During the quarter, the Inventory account on the balance sheet increased from $84.679bn to $87.225bn, a jump of $2.546bn, despite an additional 13 aircraft delivered over the same period last year.

$433m of that increase is attributed to an increase in the amount of deferred production costs (DPC) on the 787 program added to Inventory during 1Q2026.

Tooling amounts dropped slightly by $18m, while the DPC went up by $451m or ~$30m for each aircraft handed over. This indicates that, despite an increase in delivery tempo, the program is still incurring costs well over the revenue generated by each aircraft sold.

Boeing CFO Jal Malave was asked about 787 deferred production costs increasing and said, “As far as differential profile and deferred production, we had a cost-based extension. So, we added to the block, which is a good thing. At a higher margin addition to the block, it’ll take us maybe a year or so to stabilize that and start working it back down.”

Program accounting allows Boeing to accrue those increased costs in Inventory and slowly expense them on the income statement over the life of the program.

All three commercial aircraft programs accrued increases in their respective deferred production balances during the final quarter of 2025. Combined with the difference between unit-cost figures and the reported loss for 1Q2026, indicates that all three programs are operating in the red.

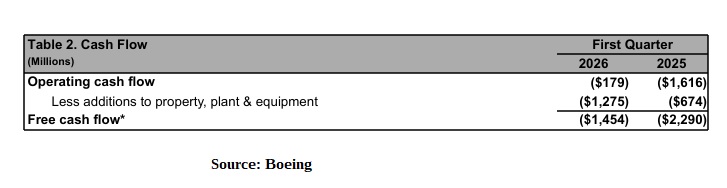

Boeing expects free cash flow (FCF) usage to level out in the second quarter and stands by its projection of $1bn-$3bn of positive FCF generation in FY2026.

Related

source